Reflections on Market Trends: How Good Were We Really?

In a retrospective analysis of the financial landscape since the Great Financial Crisis (GFC), it becomes evident that investors may have significantly underestimated the resilience of the market and the returns it has generated over the last decade and a half.

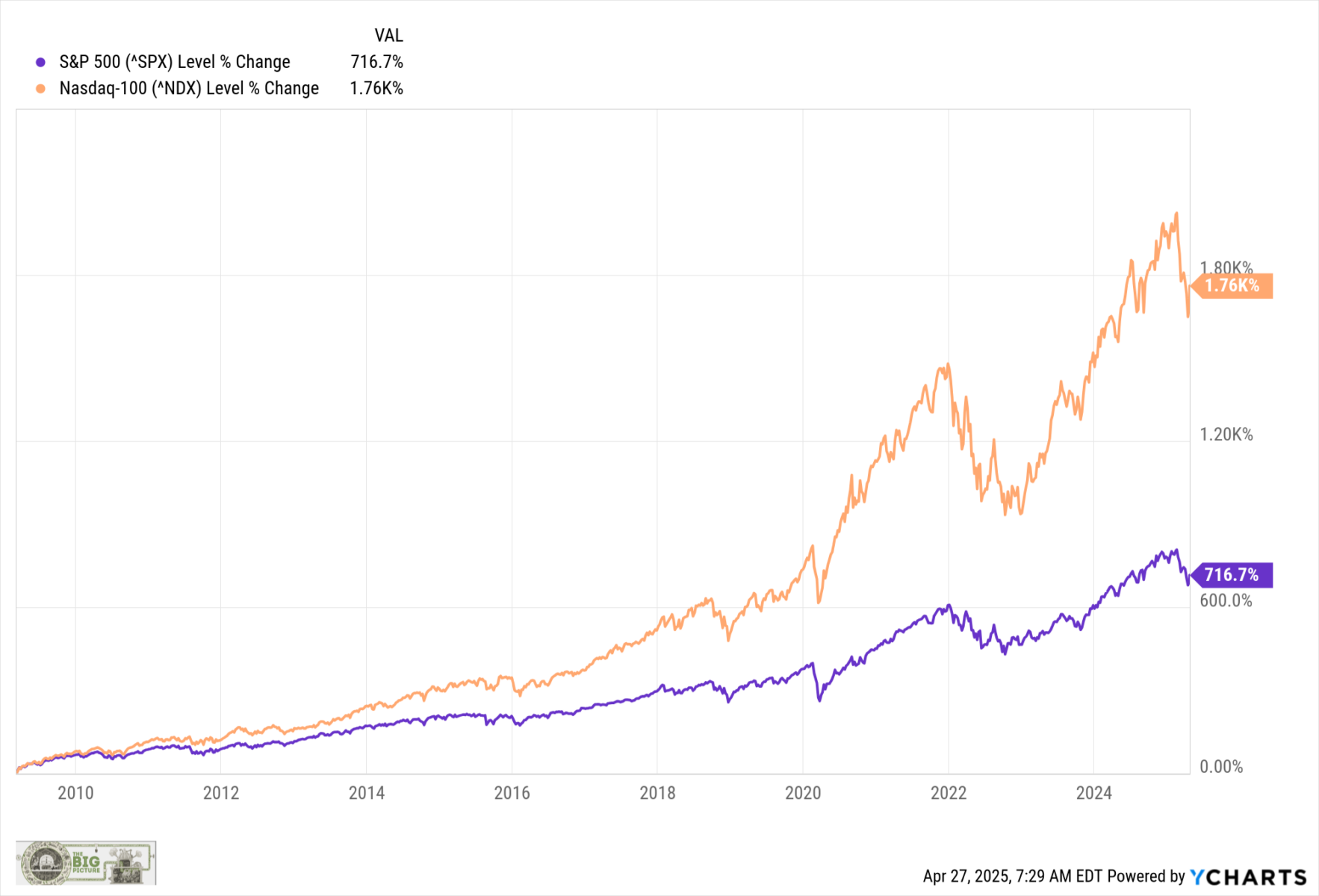

Starting from January 1, 2010, the S&P 500 has achieved a staggering total return of 566.8%, translating to an annualized return of approximately 13.3% through the first quarter of 2025. In the same period, the Nasdaq 100 has nearly doubled that performance, showcasing the robust recovery and growth within the tech sector that characterized this era. While the chart referenced in the discussion originates from March 2009, it serves as a reminder of the market's strong resurgence.

When juxtaposed against average returns over the past century, which hover around 8.7% for 15-year periods and about 10.4% annually, the current era stands out as exceptionally lucrative. Notably, the only two periods that outshine the present returns are the immediate post-World War II phase leading up to May 1957, which averaged around 18% annually, and the tech boom of the late 1980s and 1990s, peaking in April 1999 with returns near 17% annually. The current 15-year peak, noted through February 2024, hovers around 16%, indicating that investors have been riding an unusual wave of market growth.

Throughout the post-GFC recovery, equity markets experienced only minimal disruptions, despite several notable setbacks. Events such as the Flash Crash of 2010, a modest 2.1% gain in 2011, a mere 1.4% gain in 2015, and the significant drop of 4.4% in 2018, which included an alarming 20% decline in the fourth quarter, highlighted that while the road has been bumpy at times, the overall trajectory has remained positive. The onset of the pandemic in early 2020 saw a sharp decline of 34%, while 2022 closed with an 18% dip. Yet, these minor blips have not deterred overall investor confidence.

As a result of this prolonged growth, individual investors, or "Main Street," have become adept at the strategy known as Buy The Dip (BTFD). This phenomenon can be attributed to a psychological effect known as the Recency Effect, where investors have been conditioned to expect and benefit from a rising market. The combination of increasing equity values and historically low interest rates until 2022 has fostered a culture of wealth accumulation through consistent investment in the stock market. Notably, Nick Maggiulli's book, Just Keep Buying, makes a compelling case for this systematic approach to building wealth over the long haul.

The term 'muscle memory' in the investment landscape refers to the ingrained habits developed through repeated exposure to market gains. For investors, breaking away from this pattern may depend on how they respond to changes in the market environment, particularly concerning losses and rewards.

Reflecting on past market transitions reveals that investors have historically found success in purchasing during downturns. For instance, the 1980s and 90s rewarded dip buyers despite significant events such as the 1987 crash, various geopolitical tensions, and economic challenges. For two decades, investors learned to trust that every dip would eventually yield returns.

Changing entrenched behaviors is a gradual process. The aftermath of the dot-com bubble, marked by a significant downturn from 2000 to early 2003 when the Nasdaq 100 plummeted by nearly 83%, serves as a cautionary tale. During that tumultuous period, the market did not decline in a linear fashion, illustrating the unpredictable nature of equities.

One might argue that the current market environment has been too favorable for too long, although it may not have felt that way at certain moments. In October 2009, the strong market rally was dubbed The Most Hated Rally in Wall Street History, as the S&P 500 surged by 57.5% in just seven months. History indicates that substantial market corrections, such as a 56% drop, often present prime opportunities for fresh capital to enter the market. The psychological burden of recent downturns, however, has led many investors to remain skeptical, even when the market shows signs of recovery.

Over the last 16 years, the collective memory of past market pain may fade, leading to complacency among market participants. Sudden, significant daily rallies that rise by 12.5% are not typical behavior for rational traders, suggesting that the current market dynamics may be uniquely fragile.

As we reflect on this period, it is clear that the BTFD strategy has been remarkably successful, perhaps too much so. There is a risk that should trends reverse, some investors may find it challenging to adapt. This would lead to discouragement when confronted with the realization that investing for long-term growth requires a perspective that spans decades, not merely months or quarters.

Interestingly, the rising stock market was met with skepticism in the early 2010s. The current mindset is that, due to the Recency Effect, investors may no longer harbor the same level of skepticism needed to navigate potential market corrections effectively.

UPDATE: 3:21 PM April 28, 2025

Goldman Sachs has recently highlighted the persistent buying by retail investors as one of three significant positive indicators for the US stock market. This trend suggests that retail traders are playing a crucial role in supporting stock prices, and their confidence remains strong, likely unaffected unless unemployment rates begin to rise. This observation coincides with the recent surge in well-known stocks, including a remarkable 29% increase in Palantirs stock during a brief period from the announcement of reciprocal tariffs on April 2 until the market close on Friday. Along with Palantir, other major players like Netflix and CrowdStrike have also seen notable gains. According to Managing Director John Marshall, this unyielding retail demand is a key factor in the current market dynamics.

As we navigate through these uncertain times, the lessons from history serve as a valuable guide for both seasoned and novice investors alike.